Manufacturing has always been the backbone of the U.S. economy. In recent years, however, its status as an economic powerhouse has seemed to be threatened. In 1953, the industry made up over 28% of the country’s gross domestic product (GDP). In 2015, on the other hand, it dropped to just 12%.

Because of these trends, many pundits and economists wrote off manufacturing — but they were wrong. After decades of decline, we are in the midst of manufacturing growth once again. Today’s boom is set to provide untold economic opportunities due to increased productivity, the best of which will likely come to manufacturing leaders who understand it and use it to their advantages.

Building a higher GDP

Amid the aforementioned growth, manufacturing job numbers have declined in recent decades whereas wealth has not. In the last ten years — even amid the economic recession — the world has seen a 27% increase in wealth, the end result of which has been higher demand for products. With proper investment, this increased global demand could revitalize American manufacturing.

And there is already an incentive for this increase: Manufacturing growth would create massive increases in economic opportunities. In fact, McKinsey & Company predicts manufacturing growth could add $530 billion to the GDP by 2025.

Manufacturing growth also creates new employment opportunities in the United States, but these will not necessarily be limited to blue-collar assembly line jobs. Instead, increases in economic value would likely result in more retail and corporate employment opportunities as well.

Manufacturing growth is happening

In spite of the skeptics, manufacturing is growing. To fully understand the reasons for this growth, it’s important to grasp misconceptions some have about the industry.

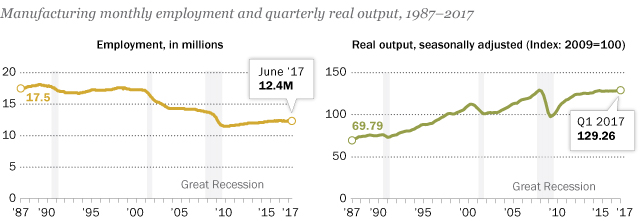

The first falsity is that a stronger industry will result in more manufacturing jobs. Instead, today’s economic strength is the result of more efficient production. According to the Pew Research Center, manufacturers produced more in the first quarter of 2017 than ever before. In spite of this, manufacturing jobs have declined consistently since 1979, paving the way for a continued shift from assembly line positions to the need for more advanced industry experts.

That means manufacturers are building more with fewer workers. While decreases in manufacturing employment are impactful, they also obscure real economic opportunities.

This is because decreases in manufacturing jobs lead to another massive misconception about manufacturing. Many assume the manufacturing industry is going overseas. Outsourcing has created very real challenges to the American economy in recent years, but the U.S. manufacturing industry still maintains massive value.

In 2016, U.S. manufacturers produced $5.4 trillion worth of goods stateside. Growth is likely to continue, so the best decision for many industry leaders is to continue investing in the sector.

Staying competitive

Projected manufacturing growth offers opportunities for industry leaders to invest in the future as their companies operate with higher efficiency, producing more economic value with less overhead.

This manufacturing renaissance is good news for plant owners and professionals. However, it also creates challenges. Manufacturers are more efficient than ever, but it’s going to take hard work and innovation for them to stay ahead of the curve in today’s rapidly advancing technological age.